Borrowers with strong credit scores typically receive lower rates compared to other loan types.

Down payments as low as 3 – 5% are possible, depending on credit. Borrowers who put 20% or more down can often avoid PMI entirely.

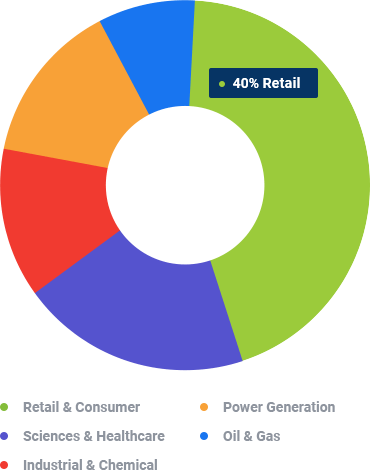

Conventional loans remain the most widely used mortgage option in the U.S., offering flexibility, competitive rates, and accessibility for a broad range of borrowers. This section provides key statistics and visual insights that highlight borrower trends, loan qualification standards, and the financial advantages of choosing a conventional mortgage.

From credit score benchmarks and debt-to-income (DTI) limits to current conforming loan caps and down payment trends, these data points help you see how conventional loans stack up in the broader mortgage landscape. Whether you're a first-time buyer or an investor, the charts below offer a clear look into the real-world performance and borrower profiles behind today's most popular loan type.